Cross-chain Lending for Crypto, NFTs and Stablecoins

This article was originally published in Blockchain Industry Review - a Crypto Curry Club Magazine published monthly and available in soft copy and the printed version.

An Interview with Featured Contributor, VU Thanh Tung,

Co-founder and CTO of DeFi platform, Rikkei Finance

The cross chain lending platform that is open – cross chain – and accepts a variety of inputs including tokens, NFTs and stablecoins. The platform only lends – that is its core competency, and it concentrates on that without distraction. It builds in fairness through calculated interest rates, recognising that interest rates do not always go up. This interest rate calculation stops pumps and dumps and leaving last in punters penalised. Finally, the team have locked in their tokens for six months or longer, demonstrating their commitment to the project.

It’s hard to be revolutionary in a field that defines the word revolution, but some projects do just that. In this case it’s Rikkei Finance as it pushes the boundaries on DeFi and in a number of ways creates an expectation of change – for the better.

The team hails from Vietnam and is now based in Singapore. CEO, Hoa Dang, and CTO, Tung Vu, both worked together for the past decade in the same company Rikkeisoft, a fast growing dev hub with almost 1500 developers working around the clock on software projects and now specialising in blockchain and smart contracts. If you wondered where all the blockchain devs have gone, that might be the answer. It is now the biggest dev company in Vietnam and has ambitions to have 10,000 employees by the year 2025 and become one of the top Vietnamese software development companies in Southeast Asia.

Rikkeisoft morphed from software company to investment powerhouse and thence to smart contract and blockchain experts. According to Tung it was a small jump to setting up their own project; everything was in place.

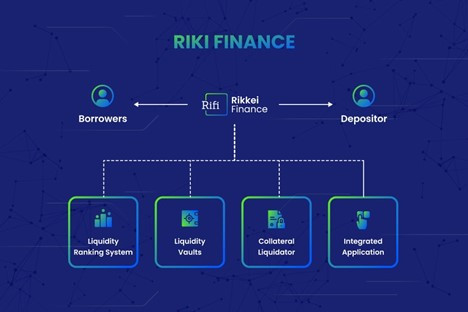

“Basically our project is open for anyone who is on the internet, but it is not limited to one blockchain such as Ethereum. It’s also not restricted to certain tokens, access or community. Anyone can take part – it’s truly open.”

Access to the protocol can be by NFTs, LP tokens, stablecoins and regular coins with the big difference that participants can use these coins or digital assets from a range of blockchains.

“We can do this as we only focus on one thing – lending – and we do it right.”

Launching a DeFi protocol in a bear market that may or not return to bullish qualities is a risk, especially when the success of the project relies on attracting investment to provide the lending liquidity.

Tung agrees it’s not easy to persuade people to put their money into a protocol during a bear run. It’s much easier during bull runs.

“Are we in a crypto winter? Hard to know to be honest but it does mean we need to focus a lot on the project and work hard. We are confident that by adding elements like NFTs as collateral and providing insurance we can make the difference.”

Rikkei Finance is not going to be an NFT marketplace, and it is not going to be an instrument protocol.

“Our focus is to be the DeFi that is secure and transparent – that is where we will earn the trust, the investment and our success.”

It’s easy, Tung argues, to attract people by offering high interest rates but that is not sustainable and can be high risk. The last investors into the project typically get stung. Instead, Rikkei Finance has done a lot of work on the maths and come up with an alternative to the linear interest model where the rate can only go up – until it doesn’t.

“When a lot of people enter for high interest rates and people borrow on the other side, something like a big price correction has the potential to dismantle the entire process and as a result the business goes bankrupt.”

Rikkei Finance uses a double threshold lending interest rate model to keep the protocol safe for everyone and attract a community looking for long term, sustainable growth.

In order to make this work, they have built a rich management system that caters for new coins to be added and also provides tangible values for those coins when used as collateral.

“Typically, stablecoins don’t fluctuate beyond 80% of their value but Ethereum can drop as much as 40% in a single day, so we need to build in ceilings. Finally people can panic too and so we need to provide security and transparency so FOMO does not negatively impact the platform.”

Tung is keen that the community has transparency on dealings on the platform – that the management system is transparent – so that they can believe in the protocol. He is also keen to promote the team, a team that is real and focused on one thing only – lending.

“And if you look at the tokenomics you will see that founders and early investors are locked in for a long time, up to six months. Only people who see this as a long term investment have got involved.”

The team has already attracted more than $5.6 million investment from people seeing this as a longterm play.

Instead of looking for fancy gimmicks to attract a community, the Rikkei Finance team has invested much time into building mathematical models such as double threshold lending interest rates where calculations are made based on where the interest rate is currently. As stress points are neared and reached, the platform can throttle back lending until such time as the borrowing and lending even out.

“You don’t want to reach a point where the interest is too low for anyone to lend or too high for anyone to borrow. Taking the linear interest model out of the equation is more complex but introduces stability which is better for everyone.”

NFT collateralization is unusual. This is conducted on a one-to-one basis, or peer to peer lending, with the owner of the NFT setting the price. If accepted, then both sides accept the risk based on that price and if the loan is not repaid, then the counterparty receives the NFT by default.

“That way the market decides the true value of the digital asset.”

The introduction of NFTs is also to link up with gamers who can use certain NFTs as assets or tokens in games. Sometimes these ingame assets can be very expensive and this is a way to loan out NFTs, receive a return, providing access to less welloff players.

Rikkei Finance has partnered with a French company to provide insurance which will kick in once the platform is live.

While the platform has already attracted significant funding, Tung and his team are not complacent. They are running bounty programmes to eliminate bugs and the majority of the funds raised will go into running the ecosystem, to provide liquidity, expand partnerships and marketing initiatives.

“We’ve hired the best PR company in the business and will be featured in all the reputable tier one business publications.”

CEO Hoa’s experience in this field came from personal dealing with DeFi sites such as Aave and Compound. He liked the decentralized nature of DeFi without possible inference from centralized players on interest rates for example.

“Having used these early, front runners I could see the value but also the limitations. However, it is very hard to change a platform that is operational and used by many people."

“I knew we needed a greenfield site to create a truly revolutionary product.”

Back to the revolutionary aspect again and it’s fair to say its hard to achieve a revolution without changing the rules. In Rikkei Finance’s case it’s all about the lending. Watch this space.